Waiting for the Other Shoe: Gen Z’s Financial Struggle and the Tools to Fix It (Op-Ed)

A Problem Hiding in Plain Sight

Every generation seems to carry its own kind of struggle. Baby Boomers often talk about building wealth during economic expansion. Millennials recall navigating the Great Recession and a shifting job market. For Gen Z, the weight that lingers behind nearly every decision often feels financial.

At first glance, their situation might not look dire. Many are splitting rent, budgeting for streaming subscriptions, or covering the occasional night out. But beneath these patterns lies a heavier reality: financial stress that feels persistent and constantly changing. As one interviewee admitted, “I’m not bad with money, but I’m always worried something will come up. It’s like I’m waiting for the other shoe to drop.”

But when will the other shoe drop? And how much will it hurt?

How We Got Here

Gen Z grew up in the aftermath of the 2008 economic crisis and amid rising education and living costs. They entered adulthood during a pandemic, stepping into a workforce defined by uncertainty, inflation, and fluctuating housing markets. For many, debt looms in the background while wages struggle to keep pace with expenses.

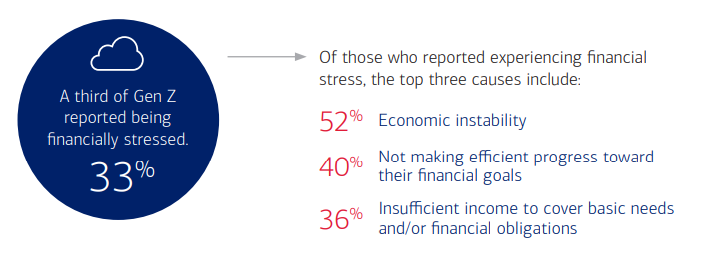

Against this backdrop, money isn’t just math it’s an emotional weight. Participants consistently expressed a divide between confidence in short-term management and anxiety about the long-term. “A third of Gen Z reported being financially stressed. Of those who reported experiencing financial stress, the top three causes include: 52% economic instability, 40% not making efficient progress toward their financial goals, and 36% insufficient income to cover basic needs and/or financial obligations” (BofA, 2025). In interviews, many described using informal tracking methods, such as checking bank statements or relying on memory, rather than structured tools.

This gap between daily stability and long-term uncertainty reflects systemic conditions shaping an entire generation’s financial approach.

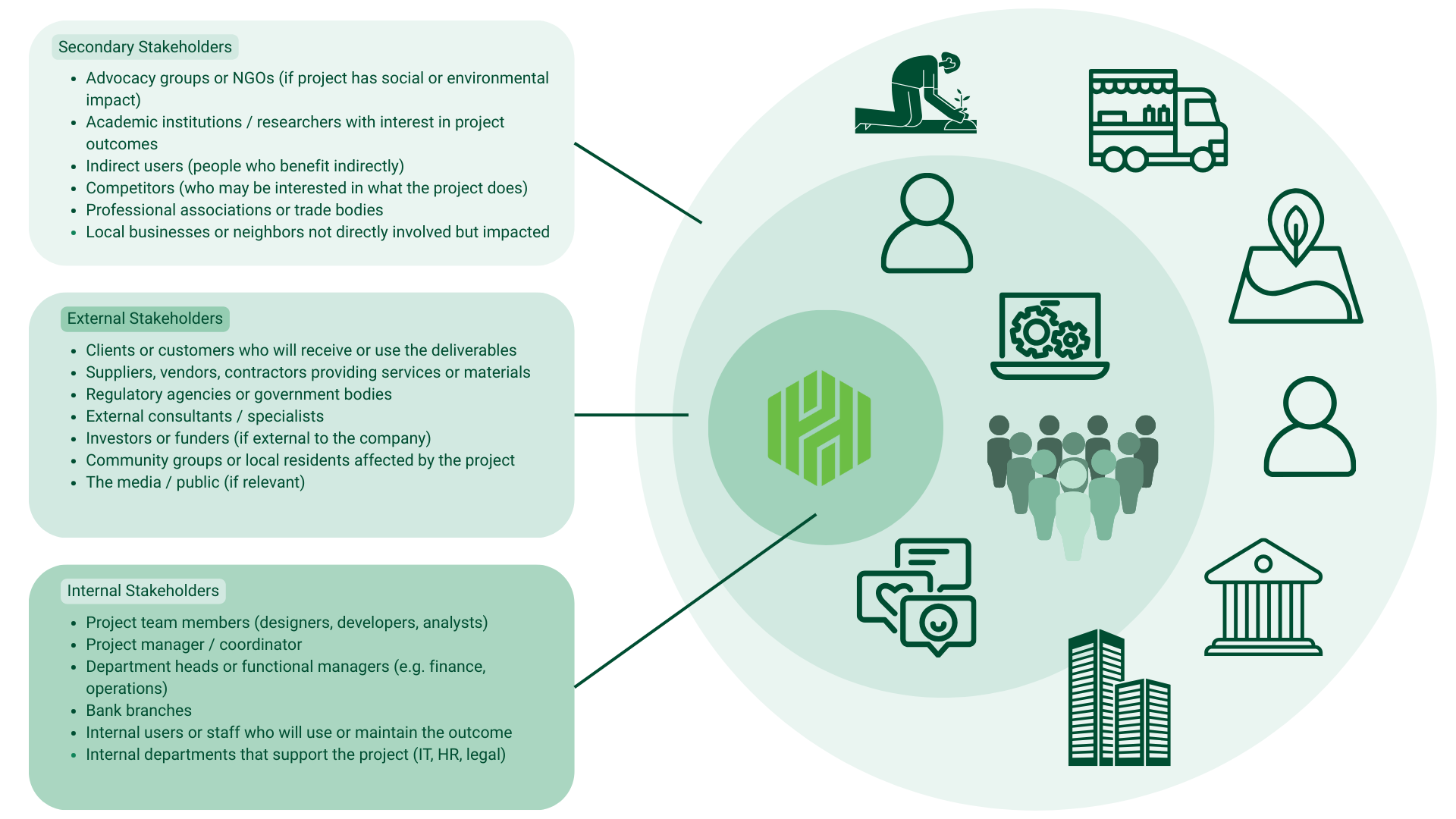

Who’s at the Table and Who Isn’t

To explore Gen Z’s financial habits, I first conducted a survey over two weeks with participants aged 18–28 from a co-ed fraternity on campus. This group was chosen for its diversity and relative representativeness of Gen Z. The survey offered a broad snapshot of how young adults manage money.

To gain deeper insight into these behaviors and the reasoning behind them, I then conducted twelve one-hour interviews with Gen Z participants aged 18–26: three college women, three women out of college, three college men, and three men out of college. I intentionally selected participants both in college and out of college to explore how financial attitudes and behaviors might differ between those still in school and those navigating post-college life. These conversations revealed more than just how Gen Z manages money, they highlighted how financial systems (and the absence of supportive structures) shape their daily life.

Beyond individual behavior, these surveys and interviews also offered a window into the various stakeholders influencing Gen Z’s financial decisions, revealing the broader ecosystem that shapes daily choices and long-term planning.

Behavioral Patterns and Systemic Gaps

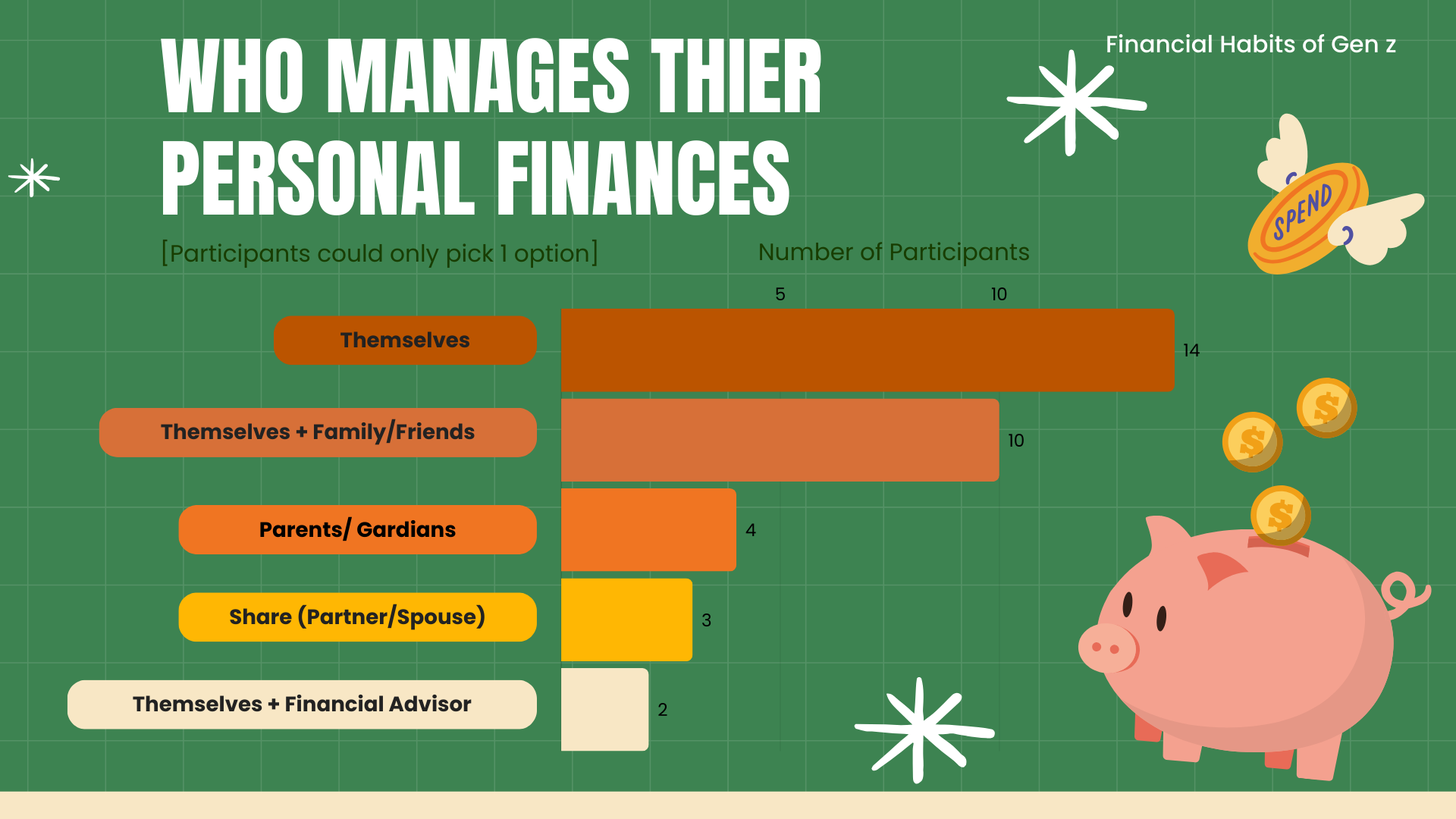

The clearest pattern is where advice comes from: family (n=11 respondents out of 12). Parents remain the first and often only source of financial guidance. This reliance suggests a strong intergenerational tie but creates a bottleneck if parents aren’t equipped with modern financial knowledge. Children risk inheriting both habits and blind spots. Few participants mentioned financial advisors, mentors, or institutional support.

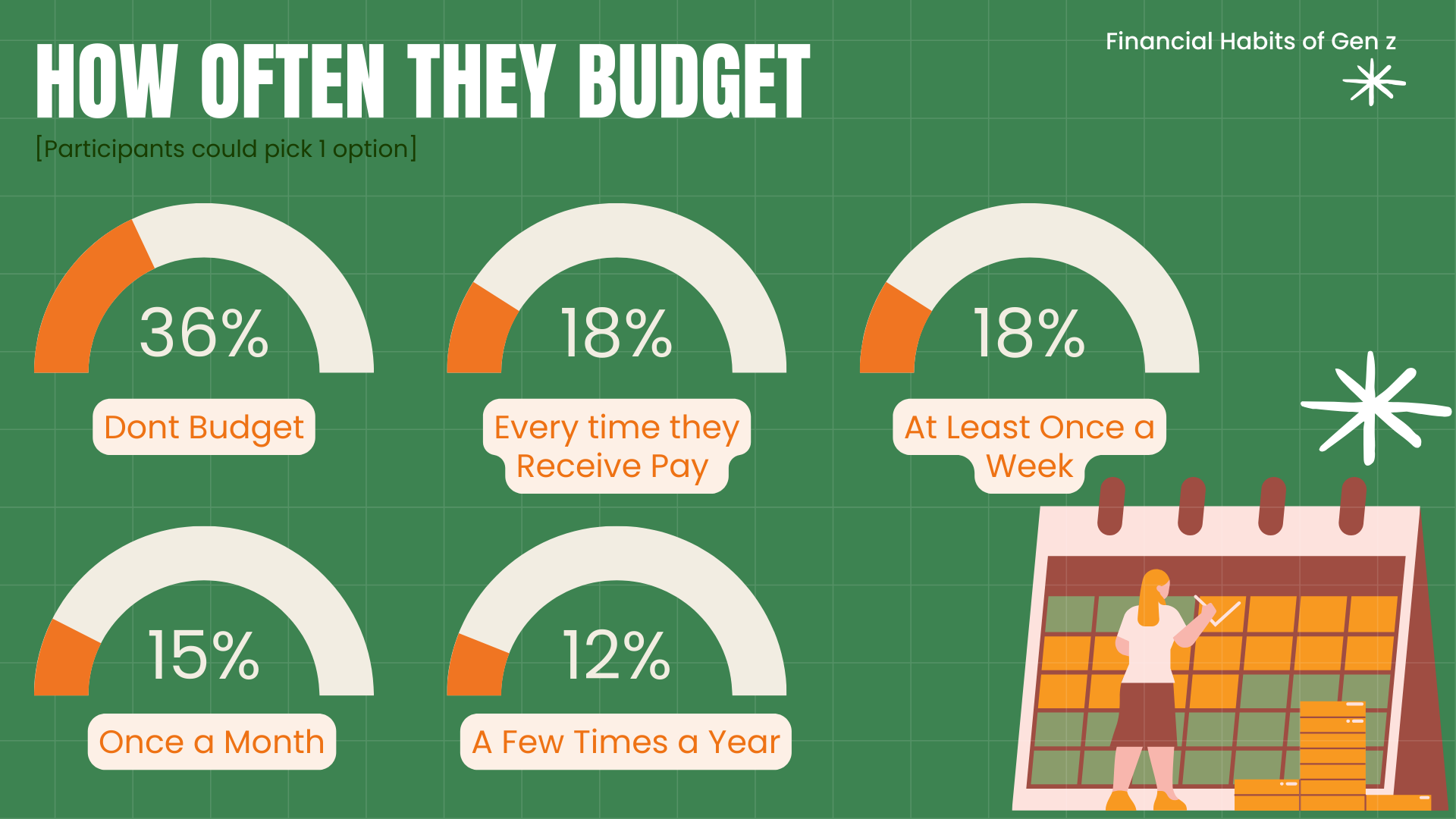

Furthermore, the tools Gen Z relies on are similarly limited. Most said they “just check their bank app (n=9)” or “mentally track” balances (n=8). A few (n=4) use budgeting tools, but rarely consistently, aligning with survey findings that 36% do not budget at all. Money management is reactive, like putting out small fires instead of building a fireproof system. The absence of schools, workplaces, and financial institutions in everyday guidance leaves a stakeholder gap, with families bearing the heaviest influence.

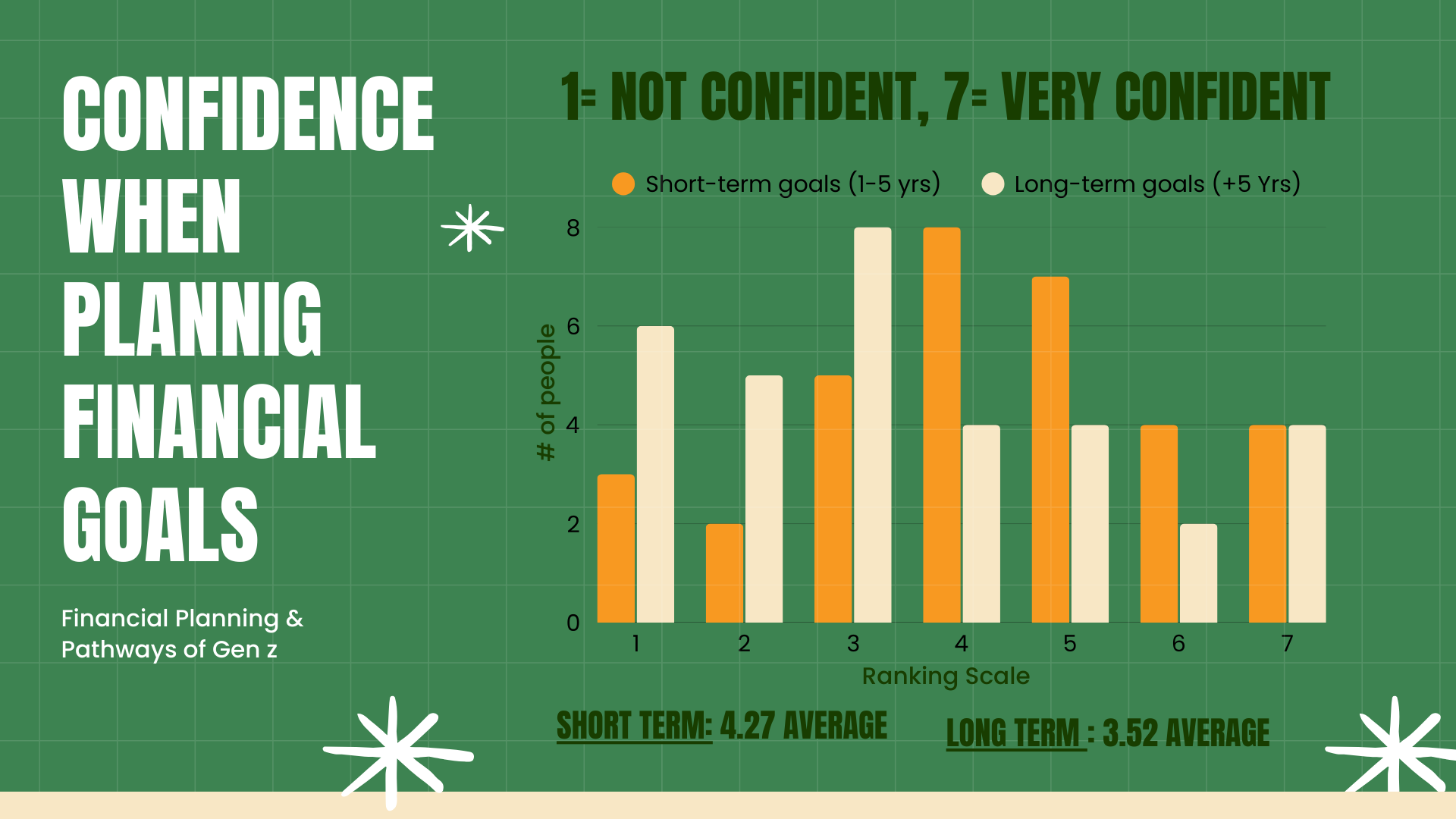

Unsurprisingly, all participants (n=12) linked money to anxiety whether about paying bills, building credit, or preparing for unknown emergencies. Even those who felt “average (n=6)” or “above average (n=4)” at managing finances admitted unease about the future. Sadly, confidence in daily transactions does not translate to long-term security. This also correlates with the survey of confidence when planning for financial goals.

The Cracks Beneath the Surface

The financial cracks manifest in behaviors. Informal tracking leaves many unclear on where money goes. Overspending often occurs not from irresponsibility, but because systems are designed without Gen Z in mind. In my conversations and research, it seems that credit cards, buy-now-pay-later apps, digital subscriptions, and digital gambling platforms are often the small, hidden ways budgets get stretched.

Gambling also appears to be a notable behavioral concern, particularly among men. In my interviews, the shift to digital platforms seemed to make gambling more accessible and woven into everyday routines, often tied to dopamine driven engagement. Literature supports this, suggesting that problem gamblers do not necessarily lack knowledge of potential harms, but struggle to modify behavior. As one review notes, “In addition to precommitments to expenditure and time-limits, pop-up messages may offer benefits as 'interrupt signals' to pause EGM games and support individuals in controlling their play” (Binde, 2014). This insight highlights the importance of understanding behavioral triggers, gender patterns, and the interaction of financial stress with risk-oriented habits.

Additionally, it seems that the shame tied to financial struggles can lead many young adults to avoid engaging with tools that could help. From my perspective, this creates a cycle where reactive habits and limited financial literacy reinforce stress. In interviews, most participants (n=8) admitted to avoiding certain accounts when feeling anxious, and most (n=8) relied solely on mental tracking rather than structured systems, showing how easily stress can shape daily money behaviors.

What Needs to Change

On a positive note, these findings point to opportunities. Gen Z doesn’t need more lectures; they need systems designed to meet them where they are. Some effective tools may be:

- Make saving fun with gamification to reward consistent habits (Gamifying Finance: Lessons from Gen Z’s Gambling Habits).

- Show and don’t judge with clear, actionable insights on financial choices (Gen Z’s Money Mindset).

- Reinforce accountability with embedded real time feedback and gentle limits (Uncommon Growth: What Business Strategy Teaches Us About Design)

- Guide with confidence through adaptive nudges and simulations to build skills (Designing for the Digital Native: Insights from Gen Z)

The following design conjectures (an early design concept used to understand the problem space) illustrate how these needs could translate into real systems:

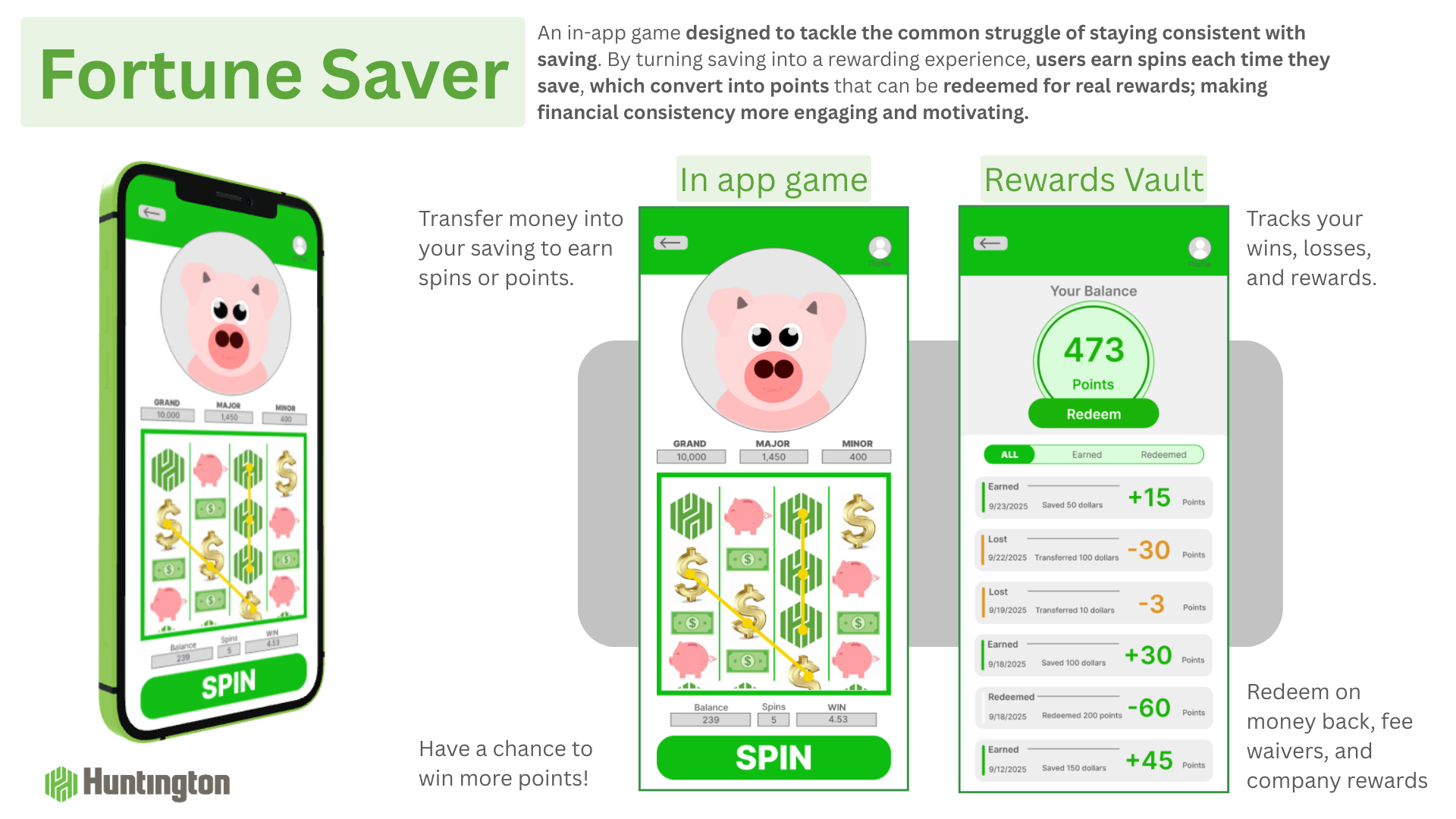

Fortune Saver

Fortune Saver gamifies saving, awarding spins redeemable for rewards each time users save. Game mechanics like points and anticipation make the process tangible, enjoyable, and habit forming. However, the gambling element raises potential risk-taking concerns, especially in users prone to dopamine driven habits. Thoughtful design must balance engagement with long-term discipline.

Questions to consider:

- Could the gamble feature lead to unintended risk-taking?

- How can rewards remain motivating without encouraging overspending?

- How might the app balance fun and responsible financial behavior?

The Money Mirror

Teh Money Mirror is an AI-powered tool that forecasts outcomes such as savings progress, potential shortfalls, and spending sustainability. It highlights app features users can leverage to adjust their financial path, fostering proactive decision making. While predictive insights are valuable, they could overwhelm users or encourage over reliance on AI without cultivating personal financial literacy.

Questions to consider:

- How can the tool present predictions without causing anxiety?

- How can users be encouraged to take action rather than rely solely on AI?

- How can the tool integrate education alongside prediction to build long-term habits?

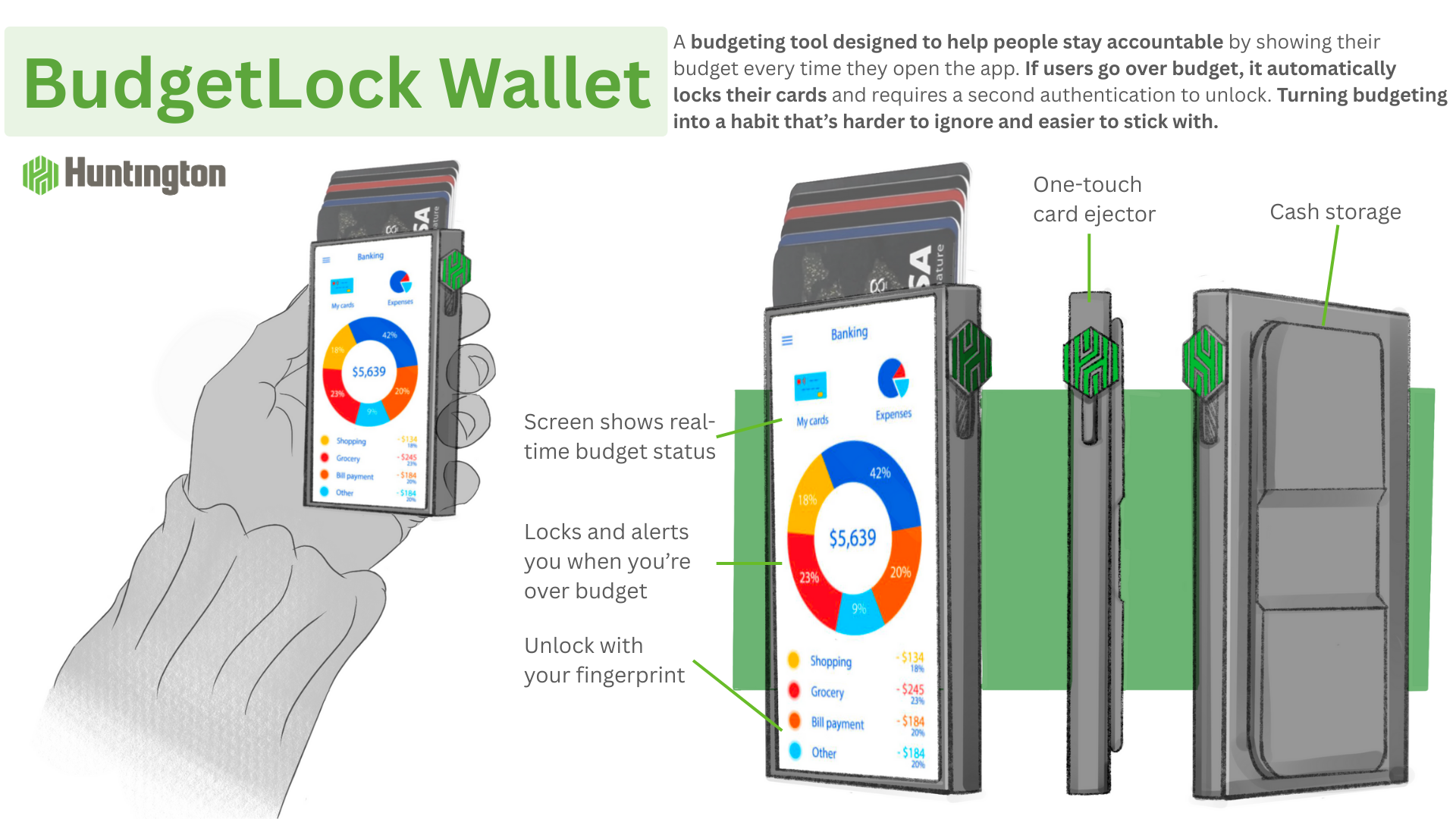

BudgetLock Wallet

This tool reinforces accountability by displaying budgets whenever the wallet is opened and locking cards if users overspend. Requiring a second authentication to unlock the cards, it turns budgeting into an active, habitual practice. Yet restrictive measures must be balanced to avoid frustration or counterproductive workarounds.

Questions to consider:

- Could automatic card locking frustrate or alienate users?

- How can the tool encourage responsible spending without being punitive?

- How might users be motivated to proactively stay within budget rather than reactively unlocking cards?

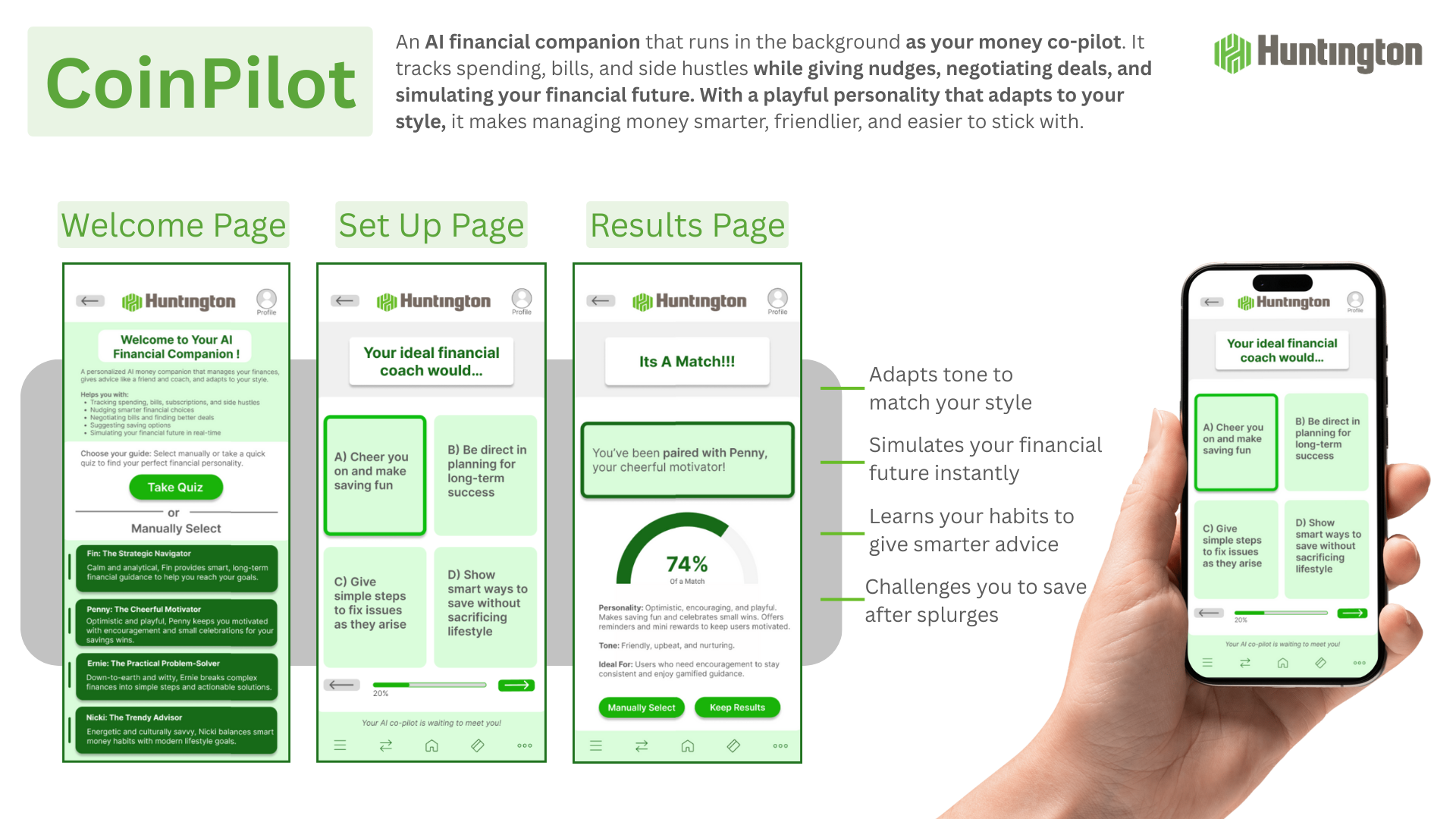

CoinPilot

CoinPilot is an AI companion that continuously monitors finances, offers nudges, negotiates deals, and simulates future outcomes. Its playful personality builds engagement, making money management approachable and confidence driven. Over reliance on nudges could encourage passive decision making, so balancing guidance with education is essential.

Questions to consider:

- How can the AI remain helpful without promoting over-reliance?

- Could playful or gamified elements encourage risky financial behavior?

- How might personalization improve engagement while supporting sound financial habits?

These design ideas tackle the gaps revealed in interviews, surveys, and literature. They also raise bigger questions: How much AI is helpful without taking control? How can tools shape habits instead of just tracking them? And how can abstract financial tasks be turned into engaging, structured, and educational experiences that encourage long-term thinking? The goal is to create designs that don’t just inform but actually help people build better habits and make more intentional financial choices.

Looking Forward

Money is often treated as a private matter, but for Gen Z, it’s a shared challenge shaped by habits, knowledge gaps, and triggers like digital gambling or BNPL apps. Interviews and surveys showed that while young adults can handle daily expenses, they struggle with long-term planning, reactive habits, and reliance on family guidance. The systems they interact with often make stress feel inevitable rather than manageable.

The next step is designing AI-powered tools that actively build financial habits while easing anxiety. Imagine apps that offer personalized nudges, micro-learning sessions, and progress tracking, turning abstract financial tasks into actionable routines that actually stick. By addressing behavior, knowledge, and system gaps together, these tools could reduce stress, foster independence, and help Gen Z navigate uncertainty with confidence. Thoughtful design should balance instant gratification with long-term goals, creating environments where managing money is intuitive, empowering, and sustainable, without waiting for the next shoe to drop.

References.

Bank of America. (2025). A window into Gen Z’s financial health: Better Money Habits Report 2025 [PDF]. https://newsroom.bankofamerica.com/content/dam/newsroom/docs/2025/BofA_BMH_Report2025_V3.pdf

Binde, P. (2014). Gambling advertising: A critical research review. Responsible Gambling Trust. https://www.gambleaware.org/media/rx3hcesz/binde_rgt_report_gambling_advertising_2014_final_color_115p.pdf

Confronted with Higher Living Costs, 72% of Young Adults Take Action to Improve their Financial Health, finds BofA Better Money Habits Study. (2025, July 20). Bank of America. https://newsroom.bankofamerica.com/content/newsroom/press-releases/2025/07/confronted-with-higher-living-costs--72--of-young-adults-take-ac.html

Google. (2025). Gemini [Large language model].https://gemini.google.com

Lilly, K. (2025, September 29). BudgetLock Wallet. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68d4a5ed48aeb40001537a60

Lilly, K. (2025, September 29). CoinPilot. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68d4a62c48aeb40001537a6a

Lilly, K. (2025, September 30). Designing for The Digital Native: Insights From Gen Z. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68c8bab66cac2000012dfab5

Lilly, K. (2025, September 29). Fortune Saver. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68d4a5ae48aeb40001537a52

Lilly, K. (2025, September 30). Gamifying Finance: Lessons From Gen Z's Gambling Habits. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68c8b9176cac2000012dfa8f

Lilly, K. (2025, September 30). Gen Z's Money Mindset. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68c8bc086cac2000012dfad7

Lilly, K. (2025, September 29). The Money Mirror. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68d4a5cf48aeb40001537a59

Lilly, K. (2025, September 29). Survey Visualization: Exploring How Young Adults Bank and Plan. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68d4a1bd48aeb40001537a27

Lilly, K. (2025, September 29). Uncommon Growth: What Business Strategy Teaches Us About Design. Ghost. https://capstone-news.ghost.io/ghost/#/editor/post/68c06fa43bd87b00016eb247

McCann, A. (2025, March 19). Generational Finances Survey. WalletHub. https://wallethub.com/blog/generational-finances-survey/133122

Note.

This op-ed draws on original reporting and context from Waiting for the Other Shoe: Gen Z’s Financial Struggle and the Tools to Fix It (Capstone News) (~40%), the author’s own analysis, framing, and argument development (~45%), and AI-assisted synthesis, drafting, and editorial refinement (~15%). All interpretations and conclusions remain the responsibility of the author.